Written by LetsBuild

Last updated October 18, 2023

Follow us

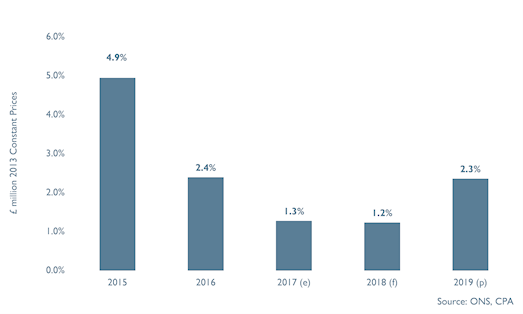

According to latest forecasts by the Construction Products Association (CPA), UK construction output is expected to grow by 1.3% in 2017, 1.2% in 2018 and 2.3% in 2019. Although the forecast presents an active post-referendum momentum, it veils a substantial discrepancy in assets across key construction sectors.

For 2019, the expected growth is seen to be primarily driven by a 28% increase in infrastructure activity and a 6.1% increase in private house building. These numbers would offset expected falls in commercial and industrial construction.

“Near-term prospects for UK construction appear bright with industry growth boosted by several new billion pound infrastructure projects across the country such as the Thames Tideway Tunnel, HS2 and Hinkley Point C and the government’s £23 billion National Productivity Investment Fund. A rise in output is expected to ensure positive growth for the UK construction industry overall if the government can guarantee it delivers on its announcements,” explained Economics Director at the CPA, Noble Francis (Francis, 2017).

As mentioned earlier, infrastructure will be the main key driving force behind the UK construction’s expansion with output forecast to increase 7.3% in 2017 and 11.1% in 2018. The high growth rates are heavily dependent on primary works occurring on high-profile projects in the water & sewerage, electricity and rail sub-sectors, such as the Thames Tideway Tunnel, Hinkley Point C and HS2 — although further delays on the following two controversial schemes cannot be ruled out (Bahra, 2017).

By the end of 2016, the UK government published a new National Infrastructure and Construction Pipeline that outlines more than £500 billion worth of planned infrastructure investment — £300 billion of which is already committed to projects by 2020–21. This followed after the chancellor’s announcement in the Autumn Statement of the new National Productivity Investment Fund (NPIF) which set out a £23 billion worth of additional investment between 2017/18 and 2021/22. However, these investment announcements are meaningless unless acted upon and have stimulated concerns regarding skills and capacity needed for the successful delivery of said investment projects.

One key source of output growth would be house building with private projects rising at 2% per year between 2017 and 2019. Noble Francis adds,

“The UK construction industry prospects should also be boosted by a positive outlook from major house builders, who appear willing to increase supply as they take advantage of rising house prices in an undersupplied market. The exception to this is the high-profile niche of prime residential in Central London, where there is already an oversupply of properties and sharply falling prices, which we expect to persist over the next 12–18 months. Substantial risks to growth remain however as the fall in the value of Sterling is leading to increased import and raw materials costs. On the demand side, while the uncertainty post-Referendum has not impacted activity on site as yet, it appears to be affecting areas that require high upfront investment for a long-term rate of return such as commercial offices and industrial factories. Both have seen new contract awards fall and this is likely to feed through into falls in sector activity from the second half of this 2017. Despite these concerns, infrastructure and private housing are anticipated to ensure that the construction industry grows between 2017 and 2019, providing an extra £5.3 billion of economic activity for the UK construction sector and wider UK economy.”

Although infrastructure investment continues to prevail as the most important political construction agenda, private housing also serves as a stimulus to UK construction output growth. Even though the housing market was warped by stamp duty changes last year, government policies like Help to Buy, low-interest rates and robust house price growth, have helped private residential to rise by 7% in 2016. With these market essentials that support housing demand, private residential is estimated to grow up to 3% this year, followed by 2% in 2018 and 2019.

Due to Brexit-related uncertainties, commercial and offices construction output has declined in the second half of 2016 and is forecasted to fall by 1% this year and 12% the following year. Nevertheless, building activities remain high in London and across other regions including Manchester, Birmingham, Leeds, Sheffield and Cardiff, which reflects a high demand for top space particularly from the technology, media and telecoms (TMT) sector. However, there seems to be a slowing down in tenant demand according to industry survey reports which hint on a downward impact post-referendum on new UK construction and development decisions that will most likely linger in the near term.

For the retail subsector, an 8% fall was experienced in 2016 with an output forecast to fall 4% in 2017, and 2% 2018 as household spending power is significantly affected by the rising inflation. This significantly curbs the demand for retail premises with ongoing structural projects favouring warehouse spaces instead.

Industrial factories construction is also expected to dwindle over the next three years due to the 2016 fall in new investment. Although the Sterling depreciation provides a boom for UK exporters, higher energy costs limit the net benefits for manufacturers. Activity in this subsector is predicted to decrease by 5% in 2017 and 4% in 2018.

The weak currency exchange rate post-referendum has increased costs and reduced contract awards in the short term. Looking at the long-term, Brexit-related issues will continue to linger and may unravel a whole new set of challenges ranging from trade terms, labour movements, regulations and standards with impacts yet unknown. Regardless, the UK construction industry is set to grow by 4.9% come 2019.

Construction output growth (%)

However uncertain the atmosphere feels right now in the UK, the UK construction sector is still set to expand over the coming years. It is imperative to be even more time and cost efficient when it comes to building projects to compete in the current market.

Whether you have infrastructure projects or doing private housing or competing in the retail and industry subsectors, here’s an ebook to boost your construction productivity. To have a greater understanding of the UK construction industry, complement this article with a feature on what BIM and Geospatial Technology can mean for UK construction. You might also want to check out the write-up on UK’s BIM Level 2 mandate.